In an increasingly competitive and globalized world, innovation represents an important role for the success of businesses and for the development of any country. Thus, the Brazilian Government has been carrying out important actions to improve the national innovation environment and through these initiatives, important Global R&D Centers have been installed in Brazil.

Brazil is now the seventh largest economy in the world and the fifth country to receive more foreign investments; Brazil has been increasing its investments in technological infrastructure, in the qualification of its professionals and improving continuously the legal framework and instruments to encourage innovation.

On this site you will find information about what Brazil has to offer to companies interested in installing their R&D centers in the country. In addition, the Brazilian Trade and Investment Promotion Agency (Apex-Brasil) offers a customized service providing market information, national legislation linked to innovation, types of financial aid.

The service is articulated, involving other federal bodies related to innovation, such as the Ministry of Development, Industry and Foreign Trade - MDIC, the Ministry of Science, Technology and Innovation - MCTI, the National Bank for Economic and Social Development - BNDES, the Brazilian Innovation Agency-FINEP, the National Council of Scientific and Technological Development - CNPq, among others.

Brazil and Agribusiness

Modern, efficient and competitive, Brazil has become one of the world's largest producers and exporters of agricultural products over the past two decades. Productivity gains, efficient management, research, innovation and technological development have revolutionized agribusiness in the country. The growth in agribusiness results from a combination of the fact that the country has the greatest area of arable land in the world - 388 million hectares (almost 960 million acres) and the increased demand for food from the world's growing population, which is expected to reach around 9 billion by 2050. Brazil has attained leadership in agribusiness due to favorable economic conditions and long-term investment in research on tropical agriculture technologies and techniques. Its climate is favorable to agricultural activities, with much of the country receiving over 1,200 mm (47.2 inches) of rain a year and abundant sunlight. These factors allow for two crop cycles per year, without the need for irrigation in some regions.

Brazil's Agricultural Model

Agriculture in Brazil is extremely diverse, ranging from small farms to large estates. A considerable part of Brazil's agribusiness is organized into cooperatives, especially in the Southern region. Family farms also play a key strategic role and are responsible for nearly half of the domestic production of corn and over a third of the coffee consumed in the country every year. Additionally, large international groups like ADM, Agrium, Bunge, Cargill, Louis Dreyfus and Syngenta have established significant operations in Brazil.

Commitment to sustainable agricultural development

Brazil has an area of 851 million hectares, of which only 38.7% is agricultural land or pasture; 61% of the country's territory is covered by native vegetation, which corresponds to 517 million hectares.

Brazil's agribusiness is unique in that it is compatible with sustainable development and environmental conservation, and the country's government is committed to promoting sustainable economic development and preventing illegal deforestation. As a result of the government's initiative to protect the Amazon rainforest, in 2009 Brazil recorded the lowest rate of deforestation in the past 20 years. The Brazilian Forestry Code, which comprises the relevant federal legislation, is one of the strictest in the world. The code was updated in 2012. Additionally, Brazil has low carbon emissions when compared to the largest agricultural producers in the world.

Food Security

The concern for food security has drawn investments to the industry and the issue has been a priority for both the public and private sectors around the world. The world's population grows as the availability of arable land decreases. Increased productivity has not been able to keep up with the increased demand for food. Over the past 10 years, for example, soybean production increased by 0.8% while demand for the crop increased by 3.4%. Similarly, corn production increased by 1.3% while demand increased by 3.6%. To meet global demand in 2025, it is estimated that soybean and corn yields must increase 120% and 360% respectively. At this rate, in 10 years, we will need twice the Brazilian production to meet the demand for these crops.

Asia plays an important role and has a special interest in food security. The region is home to 51% of the world's population and accounts for 19% of the world's gross product, but only has 18% of the world's available land and 23% of its renewable water resources. Asia also accounts for a significant portion of global consumption: 28% of the world's poultry, 20% of its beef, 31% of its dairy products and 37% of its sugar. Furthermore, Asia's middle class is the fastest growing in the world and in the coming decades its demands will be the highest in the world for that social class. In 2020, 66% of the world's middle class population will be in Asia and will account for 59% of the world's consumption.

The increase in cultivated land must be accompanied by advances and investments in agricultural technology. Fostering the development of new technological solutions to increase the productivity and competitiveness of Brazilian agribusiness is an essential part of overcoming the challenges of global food supply and is an attractive investment opportunity for foreign investors.

New Investments in Logistics Infrastructure to Supply the World

Investment opportunities are not just found in the production processes. There are also opportunities in the logistics infrastructure for the transportation of agricultural products, which is currently facing many challenges. The elimination of infrastructure bottlenecks tends to significantly benefit Brazilian agribusiness and the country's position as a major food exporter and supplier.

The number of containers transporting agricultural products handled by the import and export infrastructure in Brazil is low compared to the overall cargo. Seaports in Brazil and throughout the Southern Hemisphere are still not equipped for large ships. The agricultural expansion in the country was not accompanied by investments in the infrastructures for ports, warehouses and grain transportation, resulting in an imbalance between the production and the transportation logistics processes. The industry's growth over the last decade has revealed critical flaws in Brazil's infrastructure. The lack of infrastructure is especially critical in the Central-West, North and Northeast regions of Brazil. Today, around 58% of grains are produced in the Center-North of Brazil, but 83% of port activities take place in the Southeast and South of the country.

To improve the business environment and private investment opportunities, the new 2013 Ports Act encourages private investment in the industry, thereby promoting increased competition within and between ports to significantly increase the services offered. It sets forth guidelines for bids on new leases and the renewal of existing leases. The Ports Act also plans for improved integration between the different modes of transportation while taking into consideration the production chains and their logistics needs.

Additionally, Federal government programs, such as the Growth Acceleration Program and the Investment in Logistics Program, are building new transportation networks and logistics infrastructure. These initiatives will further boost the development of new agricultural regions, allowing producers to have their crops transported efficiently to consumption centers and to export ports in the country. Brazil's main export markets for agricultural products are the European Union, China, the USA, Russia and Japan. Thanks to innovation and excellent growth, Brazil's agribusiness does not depend on government subsidies to be competitive. According to the OECD-FAO Agricultural Outlook 2010-2019, "Brazil has the fastest growing agricultural sector by far and is projected to increase production by more than 40% by 2019 when compared to the analysis of the 2007-09 period." Brazil is currently the world's leading supplier of a wide range of agricultural products, including meat, orange juice, soybeans, sugar, tobacco, coffee, ethanol, poultry and cellulose.

The Brazilian automotive sector, which accounts for 23% of the country's industrial GDP and 1.5 million jobs in the productive chain, has developed in the country since the 1950s, with a large contribution of investments from foreign companies, gathering traditional players of European origin and new incoming companies from Japan, South Korea, and China.

In 2015, Brazilian car production and sales reached 2.43 million and 2.57 million vehicles, respectively, making it the ninth largest producer and the seventh largest global automotive market. The plants of Asian automakers accounted for roughly 25% of licensed vehicles in the period, compared with 11.9% in 2011, reflecting a decentralization in Brazilian market dynamics.

Following this movement towards internationalization, Asian auto parts and components companies foresee several investment opportunities in Brazil.

OPPORTUNITIES FOR COMPANIES IN THE AUTOMOTIVE SUPPLY CHAIN

PROXIMITY WITH BUYERS

In the automotive sector, proximity can strengthen the long-term relationship between suppliers and their customers, creating strategic advantages that may increase integration and sales. In this sense, Brazil is a mandatory market for auto parts and components companies looking to set a footprint in Latin America.

|

Maker |

Country of Origin |

Operating in Brazil since |

Production capacity (units/year) * |

Plants (vehicles) |

Recently announced investments ** |

|

Honda |

Japan |

1997 |

120 thousand |

Sumaré - SP |

R$ 1 billion (plant in Itapirina, opening date to be defined) |

|

Mitsubishi/ Suzuki |

Japan |

1998 |

100 thousand |

Catalão - GO |

--- |

|

Toyota |

Japan |

1958 |

184 thousand |

Indaiatuba – SP; Sorocaba – SP |

R$ 1,145 billion (R$ 1 bi plant for engines and shift gears) |

|

Nissan |

Japan |

2001 |

200 thousand |

Resende – SP |

R$ 750 million 2016/2018 |

|

Hyundai |

South Korea |

2012 |

180 thousand |

Anápolis – GO; Piracicaba – SP |

R$ 100 million 2015/2017 (R&D center) |

|

Chery |

China |

2009 |

150 thousand |

Jacareí - SP |

R$ 350 million 2015/2017 |

|

BYD |

China |

2015 |

5 thousand chassis |

Campinas – SP |

R$ 1.3 billion 2014/2017 |

|

Foton |

China |

2016*** |

20 thousand |

Guaíba – RS |

R$ 300 million 2012/2016 |

*Estimates

** Source: Automotive Business. Report on the Investments by Car Makers in Brazil 2011/2024.

*** Estimated launch of operations

In addition to the domestic market, a manufacturing presence in Brazil allows Asian firms to access major markets in Latin America with preferential import tariffs, due to existing Economic Complementation agreements with Argentina, Colombia, Mexico and Uruguay.

There are opportunities, in particular, to address gaps in the Brazilian automotive supply chain. The list of auto parts with grant-tariff regimen that are currently imported reflects the need for local procurement of some part, which now depend on imports, thus being vulnerable to issues such as the currency exchange.

VEHICLE QUALITY

The Brazilian automotive industry focuses on disseminating quality solutions for car manufacturing, related to efficiency, fuel emissions and vehicle security. Since 2012, for instance, industrial policy requires the manufacturers to improve energy efficiency by at least 12% in all vehicles sold in the country.

Despite the slow adoption of energy efficient technologies in comparison with other countries, it has increased over the years. Changes in the regulation of the sector, as well as the need to adopt international standards for exports, tend to increase the demand and thus the local investment opportunities in technologies such as three-cylinder engines, continuously variable transmission (CVT), dual clutch transmission (DCT), higher gear ratios, double overhead camshaft (DOHC), turbo compressors, variable valve actuation (VVA) and direct fuel injection.

TAX INCENTIVES

In late 2012, Brazilian lawmakers issued the Inovar-Auto Program, which offers tax incentives to manufacturers and investors who invest in improvements to vehicle efficiency, reduced carbon emissions and increased local research and innovation efforts (Source: IHS). This law (and program) establishes tax incentives for investments in the automotive sector related to fuel efficiency and technology:

• • Up to 30% less IPI (Industrialized Products Tax), as long as the vehicles meet a series of requirements regarding engine displacement and fuel type (Source: ICCT – International Council on Clean Transportation).

The Brazilian Treasury Department estimates that automakers plan to invest US$ 22 billion in Brazil over the next three years and that the Inovar-Auto program will bring even more investments and development to the market. The program will remain in effect until 2017, so investors should act quickly to enjoy the great benefits this program has to offer.

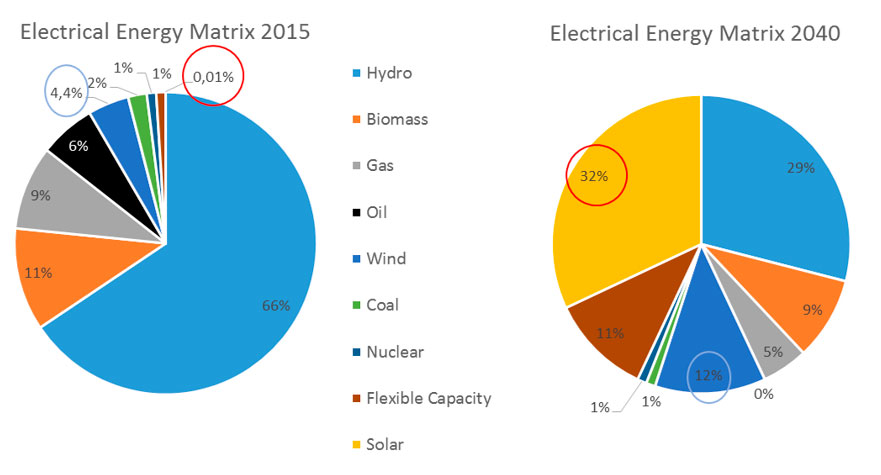

The Brazilian National Energy Plan for 2030 (PNE 2030) places non-hydro renewable energies as a key alternative to meet the growing electrical energy demand that Brazil will face in the next years, as well as to increase the share of sustainable sources in the Brazilian power matrix. Brazil is the 7th largest country in investments in clean energy, and the 6th most attractive.

Solar PV and wind energy sectors are among the most promising ones in terms of opportunities in the Brazilian economy. According to BNEF (Bloomberg New Energy Finance), the share installed capacity from these two sources in the Brazilian power matrix is going to increase from 4.4% in 2015 to 44% in 2040.

Brazil Power matrix (2015 – 2040)

Source: BNEF, 2016

Wind is now the fastest growing source of electrical power in Brazil. According to the World Ranking of Energy and Socioeconomics, in 2015 Brazil became the 10th largest wind power country in the world. In terms of new installed capacity, Brazil was the 4th largest country, only behind China, United States and Germany.

Currently, the installed capacity for wind power in Brazil is nearly 9 GW, over 5% of the Brazilian power matrix and the second cheapest source in the country, after hydroelectric power. Besides, Brazil has the largest capacity factor for wind power among all countries in the world, which reflects Brazilian competitiveness in the sector.

According to Solar and Wind Energy Resource Assessment (SWERA), Brazil ranks as the 5th country in the world for solar potential, receiving more than 4 kWh/m2 of solar irradiation each day in even the least sunny areas in the south, and over 6.5 kWh/m2 in the resource-intensive northeast region. This results in a high capacity factor for solar PV installations of between 19-24%; a factor over twice as high as the average in Germany (one of the current leaders in PV deployment globally).

By 2015, around 142 MW of PV capacity had been installed in Brazil. In 2015-2016 alone another 500 MW is expected to come online, with deployment set to increase significantly in the coming decade in response to the government pledging to contract at least 7 GW of utility-scale solar PV by 2023/24. After intensive regulatory improvements made by the Brazilian government, Distributed Generation (DG) – which consists in solar PV systems installed in residences, industrial and commercial establishments – is also expected to reach 5 GW by 2024.

BRAZIL: A MARKET DEDICATED TO THE CONTINUED DEVELOPMENT OF THE LIFE SCIENCES

A large and developed healthcare market

Brazil is a perfect location for multinationals that wish to diversify their Life Sciences activities in a large developing market where the healthcare sector is increasingly attractive for medical equipment. In Brazil's favor are the enormous size of its potential market, increasing expenditures in the healthcare sector, and an increasingly aging population:

• 33% of the 201 million Brazilian population are still younger than 20; however, life expectancy reached 74.6 years in 2012. Today, 20 million people older than 60 live in Brazil, similar to what is seen in developed markets like France and Germany.

• The healthcare sector accounts for 9% of the GDP and, according to the Brazilian Association for the Medical, Dental, Hospital and Laboratory Equipment Industry (ABIMO), Brazil spent over US$ 9.1 billion in medical equipment in 2011, which is 50% more than in 2009.

• Brazil has a solid and well-established public health program, which is responsible for 50% of healthcare sector expenditures in the country. Part of the procedures performed in this system are contracted by the private sector.

A comparison between the increase in Brazil's current population and the expenditures in the healthcare sector shows that, when expressed as a percentage of the country's GDP, these expenses are well above those of its Latin American counterparts, such as Mexico and Chile, and not far behind those of more developed countries like Canada.

Technology to drive future growth

The Brazilian healthcare sector is not only enormous, it is also growing at an accelerated pace. Brazil has overcome a number of recent crises and its rapidly expanding middle class is demanding healthcare technology, services and attention. Consumers have increased their spending on private health insurance by 50% over the past five years due to increased purchasing power and higher employment rates. These factors have resulted in an impressive performance by the medical equipment sector and this prosperity is expected to continue for the next ten years:

• Over the last five years, more than 27 million Brazilians have ascended to the middle class, increasing their spending on technology, vehicles and healthcare.

• From 2001 to 2011, per-capita healthcare expenditures have gone up by 6% around the world, 10% in Latin America and almost 14% in Brazil.

• From 2000 to 2010, Brazilian per-capita healthcare expenses have grown at a compound annual rate of 14%, reaching US$ 990.

• According to ABIMO, the Brazilian market grew by more than 9% in 2010 and roughly 18% in 2011.

The current medical equipment market is highly developed to meet current demand, with 90% of a hospital's technology and equipment needs being easily supplied domestically. A supply surplus has resulted in more than US$ 700 million in exports per year. Thus, the future growth of the Life Sciences sector will be driven by disruptive innovations and technology transfers that are currently not taking place in Brazil.

• In Brazil, over 68% of medical equipment suppliers are family-owned small and medium businesses. This presents an opportunity to market new technology products or supply existing companies that are growing and investing in better technologies.

The Brazilian environment is ripe for the introduction of more technologically advanced products and expenditures on such items are expected only to increase over the coming years.

Government Incentives Favor Local Production and Development The Brazilian public healthcare program, Unified Healthcare System (Sistema Único de Saúde or SUS), cares for 80% of the Brazilian population and is responsible for 48% of the country's current healthcare expenditures. In 2011 alone, the SUS carried out more than 740 million exams, 2.4 million chemotherapy treatments and 4 million surgeries for Brazilian consumers. Even some procedures carried out in charitable hospitals and clinics were paid for by the public healthcare system.

Considering the Brazilian government's strong involvement in the healthcare sector, the Life Sciences sector remains a national priority and an important concern. With the aim of securing sustainable supply and exports revenues, the government has developed a number of initiatives to promote foreign investments, technology transfers and the continued development of the sector as a whole.

Attractive fundraising and financing solutions have been created by BNDES (Brazilian Development Bank) and FINEP (Financing Agency for Studies and Projects) to drive foreign investment and technology development.

The government is encouraging partnerships between the public and private sectors for technology transfers and development through various public laboratories around the country. These "Production Development Partnerships" will facilitate government registration and purchase of the technology required by the Brazilian public healthcare system when this technology is developed and transferred to public laboratories.

The sector's standards and policies have been adjusted to align with internationally accepted regulations in order to better facilitate technology transfers and promote international business transactions.

• The Ministry of Health has established a number of programs to expand the SUS in order to develop specific sectors, such as radiation therapy, investing US$ 300 million in equipment, subsidies for workforce training programs, financing and materials.

• To strengthen its position, the Ministry of Health is currently developing a centralized purchasing system in order to leverage bulk purchases as a negotiation tool.

• Products and medications on the SUS essential purchases list receive priority for both patent requests and ANVISA (National Health Surveillance Agency) registry.

• The Ministry of Health regularly publishes a list of essential and priority medications, called RENAME (National List of Essential Medications) and plans to expand it to include medical equipment so that manufacturers can be aware of the most important public sector demands ahead of time.

Solid regional R&D and cluster development

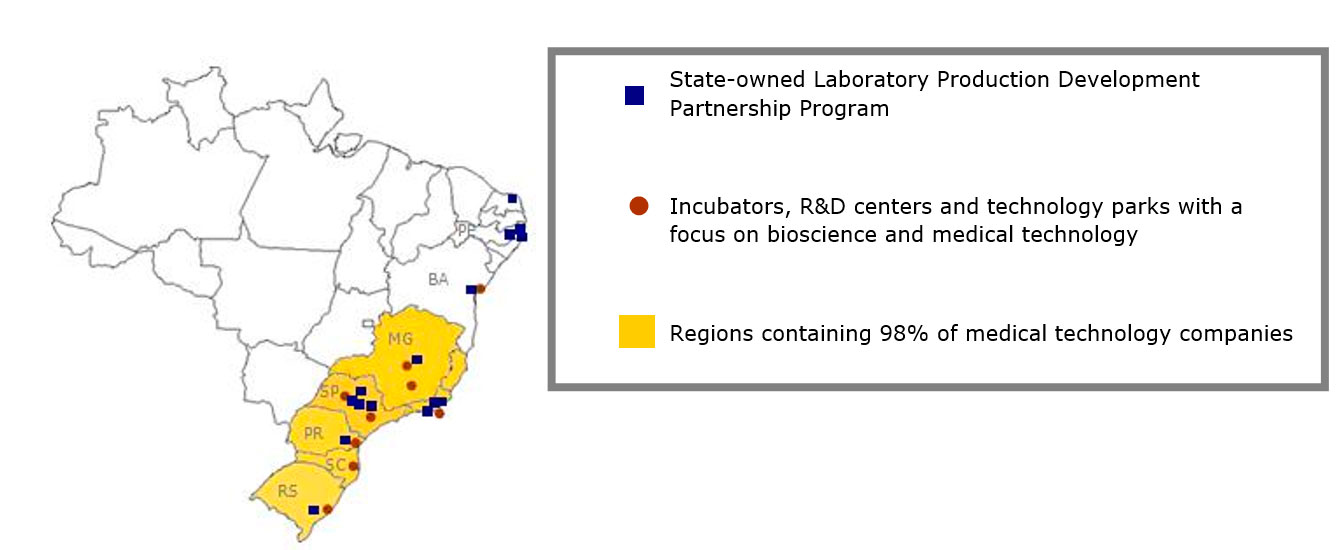

Approximately 94% of Brazilian medical products and equipment are manufactured in the Brazilian South and Southeast regions, which are also the country's main manufacturing centers; new arrivals will benefit from existing supply chains. Furthermore, several industrial clusters have developed around important public and private universities and research and development centers, such as CIETEC (São Paulo), BioRio (Rio de Janeiro), BioMinas (Minas Gerais) and FIPASE (Ribeirão Preto, SP). Developed laboratories, business incubators, high-tech production units and ties with universities combine to create an attractive ecosystem for medical equipment investments in the South and Southeast. However, state-owned laboratories, which can encourage foreign companies interested in entering the Brazilian market, can likewise be found in other regions around the country. A strong dedication to furthering R&D in Life Sciences is indicative of potential for innovation and an enormous long-term investment opportunity in Brazil.

Better Investment Opportunities in Medical Equipment

The Brazilian medical equipment sector currently produces a surplus of products in some sectors while suffering from considerable scarcity in others. Subsectors manufacturing products such as orthodontics, incubators and medical furniture, for example, successfully export to countries throughout the world and currently produce a surplus in the country. Nevertheless, the current overall negative trade balance in the healthcare sector is about US$ 1.5 billion and certain trends shift demand to areas where present and forecasted production is unable to meet local demand:

• The aging population, the increased purchasing power and the presence of isolated populations in the interior of the country are generating demand for more mobile systems, monitoring devices and home care equipment.

• Increases in purchasing power and the growth of the private healthcare industry will generate demand for new technologies and high-tech equipment, such as PET scanners, analyzers, optical instruments and X-ray machines.

• Other general needs and trends in the medical equipment sector include smaller products (miniaturization in general), advanced software, increased automation, professional radiology devices and certain consumer goods.

• The Brazilian Ministry of Health intends to regularly publish a list of priority medical equipment required by the public health system, which will allow manufacturers to plan more strategically. This is already successfully done for medications.

BRAZIL: A GREAT OIL & GAS MARKET AT A DECISIVE TIME

The Next Great Producer

According to the 2011 World Oil Outlook published by OPEC (Organization of Petroleum Exporting Countries), Brazil is poised to become one of the largest suppliers of conventional oil in developing regions, ahead of present-day OPEC countries. What factors will make Brazil the next major oil and gas producer and equipment and machinery consumer?

• Although Brazilian oil and gas production has shown stable growth since it began more than sixty years ago, recent discoveries of new oil sources promise to drive exponential growth in future production.

• Since 2007, dozens of deepwater oil fields have been discovered in the vast region off the Brazilian coast. The pre-salt basins, located under a large layer of salt more than a mile (2,000 meters) thick, extend over an area 500 miles (800 kilometers) long by 125 miles (200 kilometers) wide.

• Estimates of pre-salt layer deposits range from 50 to 80 billion barrels of high-quality oil, according to the ANP (Brazilian Oil Agency) and market analysts from around the world.

• To date, 15.8 billion barrels of recoverable oil have been found in the Lula and Sapinhoá pre-salt fields alone. According to Petrobras, Brazil's national oil and gas company, the pre-salt layer currently produces 400,000 BOE/day, or approximately 18% of the total Brazilian production.

The oil and gas (O&G) sector is a priority for the Brazilian government. The growing production, the recent discovery of attractive deposits and the possibility of unconventional oil production have resulted in changes to regulations encouraging direct investments in this market, as well as increased R&D and foreign participation in the production and supply chain.

A Long-term Investment

An investment in the Brazilian O&G industry will yield returns in the long term. The extensive deposits and fast growth forecast demonstrate a great potential for the Brazilian O&G sector, but other factors contribute to make Brazil particularly attractive to investors interested in making long term investments:

• Petrobras controls roughly 90% of refinery capacity, 90% of oil production and 25% of oil and ethanol distribution in Brazil.

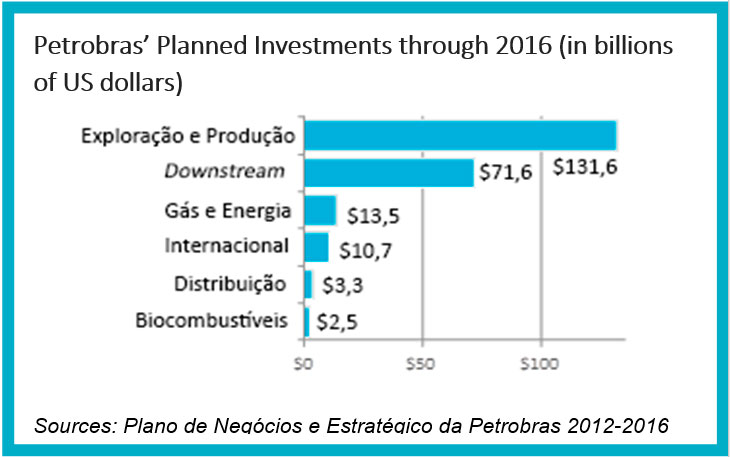

• According to the Petrobras 2014-2018 business plan, the company is expected to invest over US$ 220 billion during this period, 70% of which are earmarked for exploration and production via partnerships.

• Petrobras has published in its 2014 report, "Procurement Policy and Critical Equipment Supply," that the company alone will consume 1.3 million tons of steel for hulls, over 570 wet and dry trees, 3,667 km of flexible pipe, 338 compressors and many other products to support its aggressive production expansion plans for 2014-2018.

Local Content Requirements Favor Productive Investments

Any new IFBs from the Brazilian Oil Agency or service and equipment contracts with Petrobras will need to meet the 70% local content requirement. This is expected to not only promote strong domestic investments, but also improve post-sale services and maintenance, delivery times, and protect against delays resulting from global demand.

BNDES (Brazilian Development Bank) also requires a minimum local content certification for specific O&G financial options.

Potential for High-level Research and Development

Research and Development (R&D) have become essential in the Brazilian O&G sector, driven by the growing demand for unconventional oil, improved recovery of existing fields, cost-effective solutions for new developments in deepwater fields, and new materials for pre-salt basins.

Brazil has the technical and scientific resources to participate in innovative and high-level R&D in the O&G sector as well as qualified people with excellent experience. The major success Petrobras has had in deepwater and offshore exploration and production is proof of these advantages. Furthermore, many strategic investments and programs have been developed to provide even more support for current R&D efforts and ensure a stable flow of trained employees for the Oil and Gas sector. Research & Development (R&D)

• From 2010 to 2012, multinationals like Schlumberger, Siemens, FMC Technologies, Baker Hughes, Georadar and others have invested over US$ 150 million in Brazilian R&D centers. Other companies, such as GE Oil & Gas and EMC, have announced over US$ 700 million in planned investments in Brazilian oil and gas R&D for coming years.

• The regulations for companies participating in highly productive O&G IFBs require operators to reinvest 1% of gross revenue in local O&G, internally and externally, in local universities, and a portion of these investments is allocated to financing O&G-related scholarships. From 1998 to 2013, these funds have added up to R$ 8 billion.

Links to this sector

If you are interested in finding business partners, exporting to Brazil or licensing production, follow the links below to the major associations in this sector:

• Brazilian Oil Industry Organization (ONIP) – http://www.onip.org.br/?lang=en

• National Agency of Petroleum, Natural Gas and Biofuels (ANP) – http://www.brasil-rounds.gov.br/index_e.asp

• Petrobras – http://www.petrobras.com/en/home.htm

In a continental country such as Brazil, infrastructure is an especially relevant matter. Transportation, logistics, power generation, sanitation and housing are core issues for Brazil’s development, as well as great business opportunities themselves.

A promising scenario for investments, a clean and diversified energy matrix and some of Latin America’s biggest ports and hubs are among the things that make Brazil stand out.

Investment in infrastructure has almost tripled in the past few years, from BRL 48.6 billion (USD 15.5 billion) in 2007 to BRL 130 billion (USD 41.5 billion) in 2014, taking into account both public and private capital.

However, there is still much to be done and infrastructure remains a major priority, with several ongoing projects and financing programs. By the end of 2016, the federal government announced huge concessions and a public-private partnerships (PPPs) package that included 34 assets and services to be auctioned by 2018. Named Projeto Crescer (“Growing Project”), this package is part of the Investment Partnerships Program (PPI), an initiative launched in 2016 by the government to foster the relationship between the government and private enterprise and to stimulate a new cycle of infrastructure investments.

In March 2017, four major airports in state capitals were the first to be auctioned under the new program, raising BRL 3.7 billion (USD 1.18 billion) in 25 to 30-year concession contracts. Port terminals, railroads, power plants, mining areas and water and sanitation services are some other assets scheduled to be auctioned soon, all of which are detailed on the following website:

www.projetocrescer.gov.br/projects

.

The PPI complements the Accelerated Growth Program (PAC), a monumental program of infrastructure investments launched in 2007.

- addition to those programs, Brazil will also join the world’s largest oil producing countries in a few years’ time as it advances its “Pré-Sal” exploration. The huge offshore pre-salt oil layer discovered off the Brazilian coast in 2007 already produces 1.5 million barrels a day (as of February 2017) – more than half of the 2.8 million barrels produced nationwide. New bidding processes for unexplored areas will take place in the next few years.

BRAZIL IN NUMBERS

INFRAESTRUCTURE

▸

64,844.7 km of paved federal highways (CNT/February 2017)

▸

211,418.4 km of total paved road network (CNT/February 2017)

▸

30,576 km of railroads (CNT/February 2017)

▸

2,460 airdromes, with 63 national and international airports (CNT/February 2017)

▸

37 public ports and 180 private port terminals (SEP/2016)

▸

2.55 million barrels of oil a day (bbl/d) March (ANP)

▸

Freight transportation matrix in Brazil (CNT/February 2017):

»

61.1% road

20.7% rail

13.5% water (maritime and inland waterways)

4.2% pipelines

0.4% air

▸

Electricity consumption: 461,552 GWh

(EPE/2017 - 12-months’ consumption ending in February 2017)

▸

Projeto Crescer (English) http://www.projetocrescer.gov.br/about-the-program

▸

Petrobras activities (English) http://www.petrobras.com.br/en/our-activities/performance-areas/oil-and-gas-exploration-and-production/pre-salt/

▸

http://www.agenciapetrobras.com.br/Materia/ExibirMateria?p_materia=979101

▸

Oil auction, MME (Portuguese only) http://www.mme.gov.br/web/guest/pagina-inicial/outras-noticas/-/asset_publisher/32hLrOzMKwWb/content/cnpe-aprova-realizacao-da-3a-rodada-do-pre-sal

▸

Transportation data, CNT (Portuguese only) http://www.cnt.org.br/Boletim/boletim-estatistico-cnt

▸

Energy data, EPE http://www.epe.gov.br/mercado/Documents/Resenha%20Mensal%20do%20Mercado%20de%20Energia%20El%C3%A9trica%20-%20Fevereiro%202017.pdf

SOURCES

THERMAL POWER PLANTS: 2,949

HYDROELECTRIC POWER PLANTS: 1,262

(Aneel/April 2017)

NUCLEAR POWER PLANTS: 2

WIND FARMS: 424

SOLAR PLANTS: 44